First-time Home Buyer Loans, Grants and Programs: Learn How to Save Money When Buying Your First House

Many first-time homebuyers learn as they go along and rely on either their realtor or lender to lead them through the process. There’s nothing wrong with this, but if you don’t do your own research, you’ll likely miss out on some truly good first-time homebuyer programs (which most realtors have never heard of and most lenders aren’t fans of— but luckily neither matter).

These programs can do a lot of things, but for the most part they’ve been put in place by state governments to help people like you stop renting and start owning— to be one of the first steps towards elevating you to a higher standard of living.

So the question is: Could you use help with down payment or closing costs if you were to buy a house? Could you save $8,000 or more to buy a $200,000 house?

Think it’s too good to be true? Many of these programs are offered through local and state governments.

What are First-Time Home Buyer Loans?

First-time home buyer loans are loans that can help you cover the down payment and closing costs of your first-time home purchase. Though they are loans that have to be paid back, they usually come with deferred payments and 0% interest. Better yet, they are often even forgivable if you meet certain qualifications. Many times the homeowner often simply needs to live in the home for a certain amount of time to make the home loan 100% forgivable. If the home is sold, foreclosed, transferred, or if the homeowner moves out before the minimum amount of time has passed, the loan will then need to be paid back.

To qualify for these programs, you usually have to be below a certain income threshold. 80% AMI (average median income) is the norm, but there are other programs that are much more lenient with 100% to 150% AMI (and in California we’ve seen programs as high as 180%).

What are First-Time Home Buyer Grants?

First-time home buyer grants are similar to the first-time home buyer loans discussed above, but the homeowner is never in any danger of ever having to repay the money. These programs exist, but they are few and far between for obvious reasons.

Most programs are advertised first as loans, but have easy conditions to meet in order to make the money ‘free’.

Where do you find these programs?

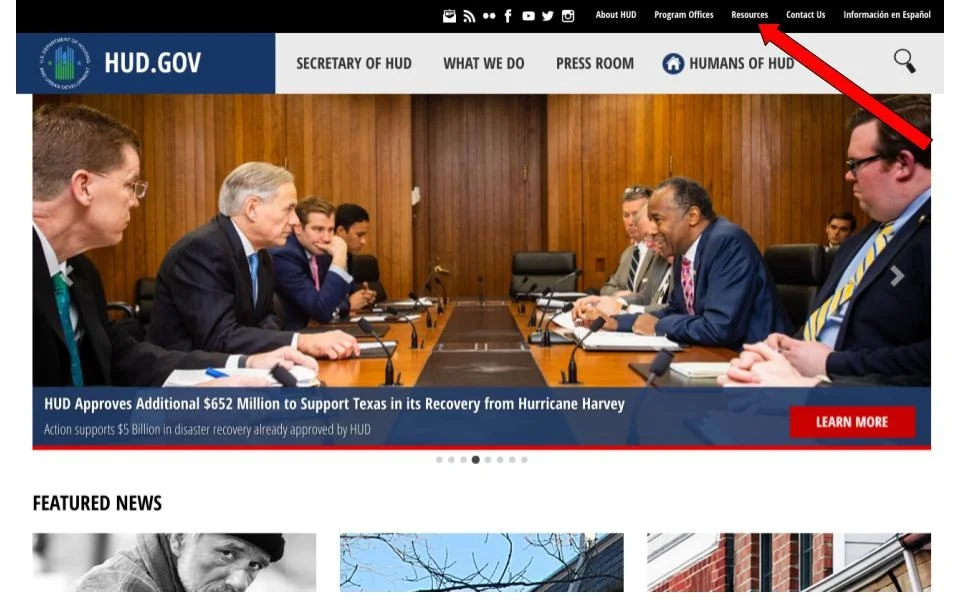

The simplest thing you can do is to go to your state’s ‘Department of Housing and Urban Development’ web page, which can be reached at www.hud.gov.

Once there, first click on Resources.

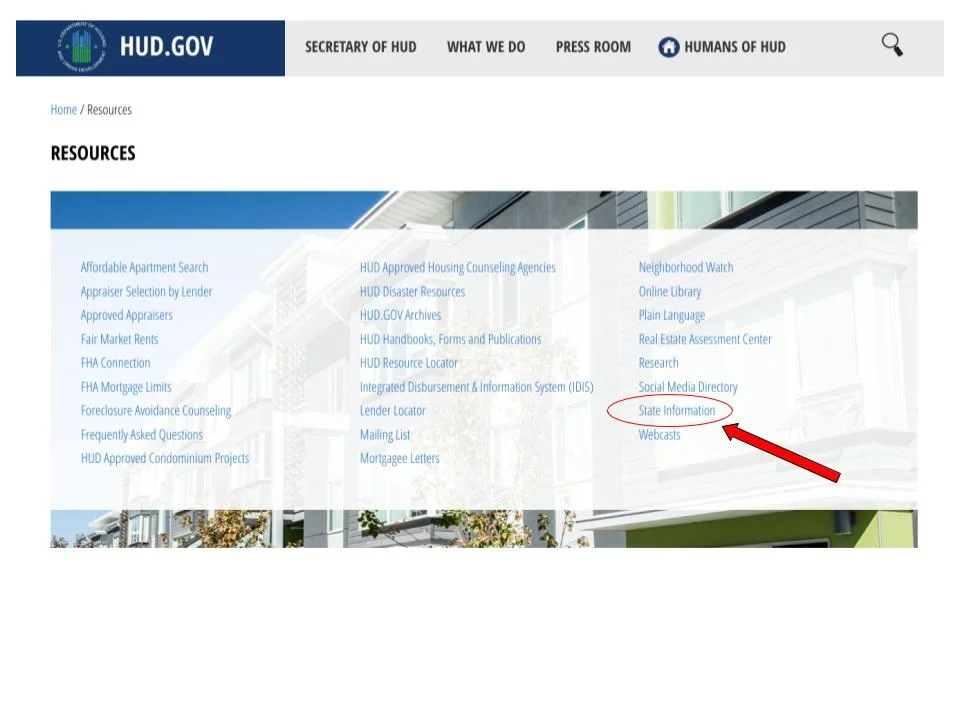

Next, click on State Information.

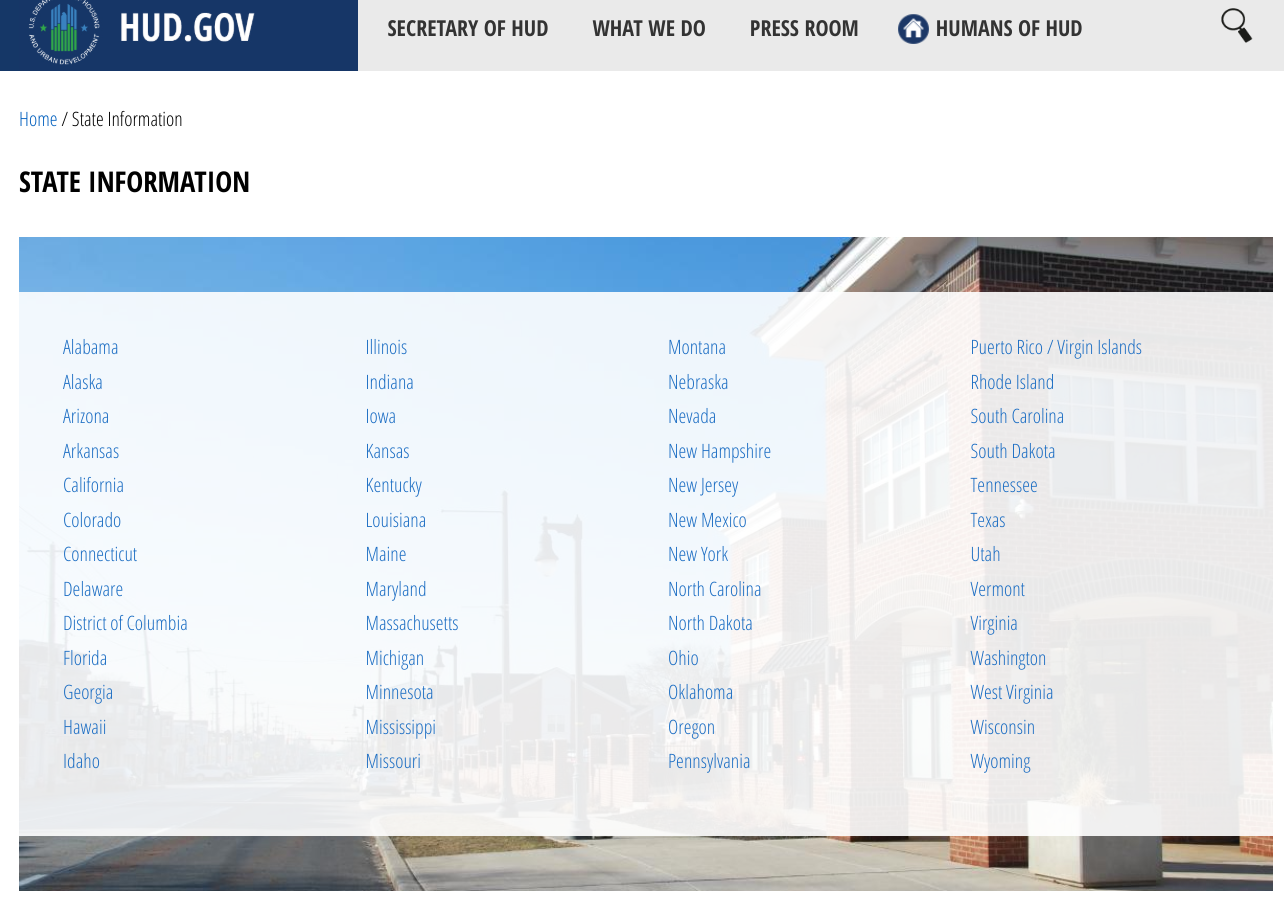

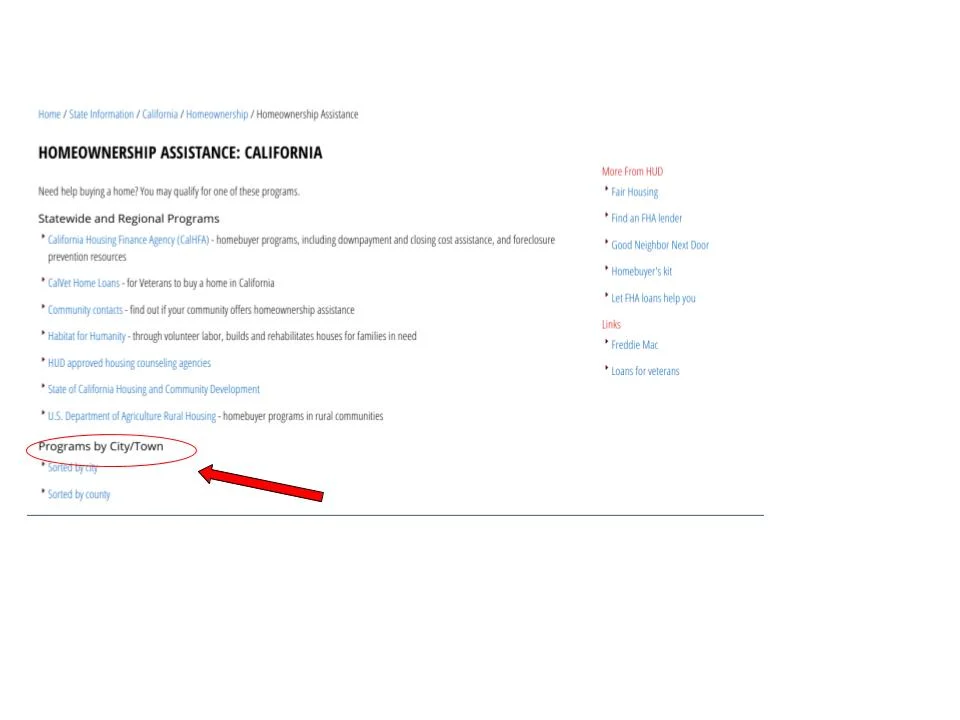

Find your state on the master list. (Note: we’ll do California from here on as an example).

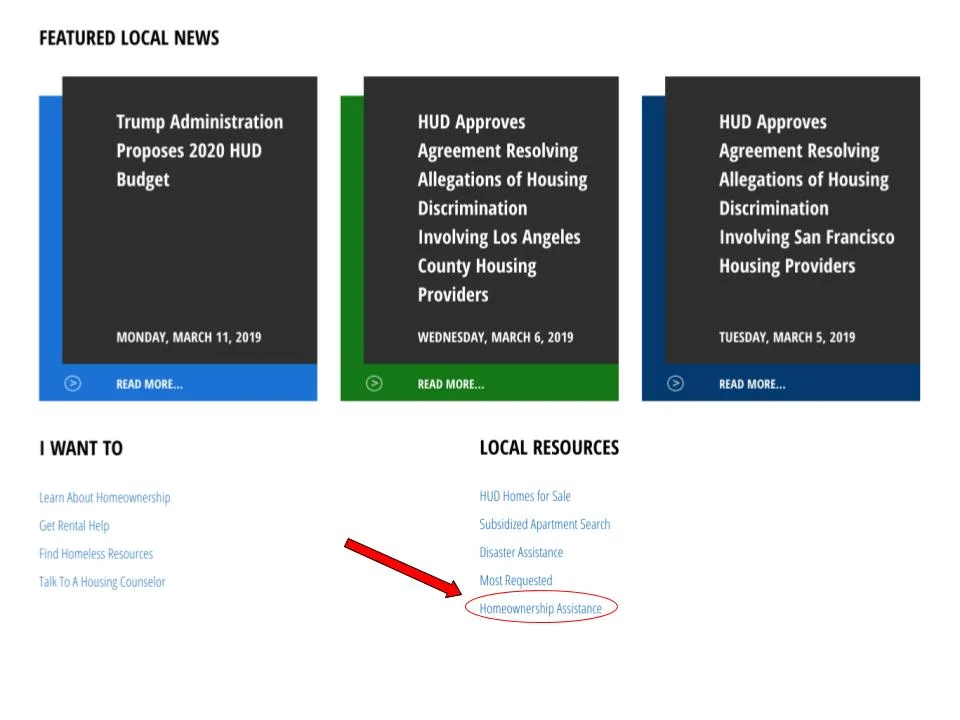

Once in your state, scroll past ‘Featured Local News’ and the ‘I want to’ sections. Find ‘Local Resources’ and click on Homeownership Assistance.

From here each state will look a little different. Because California is such a large state, you’ll notice it’s broken up into ‘Statewide and Regional Programs’ and ‘Programs by City/ Town’. If your state is like this, first look into local programs near you, by clicking on ‘Programs by City/ Town’.

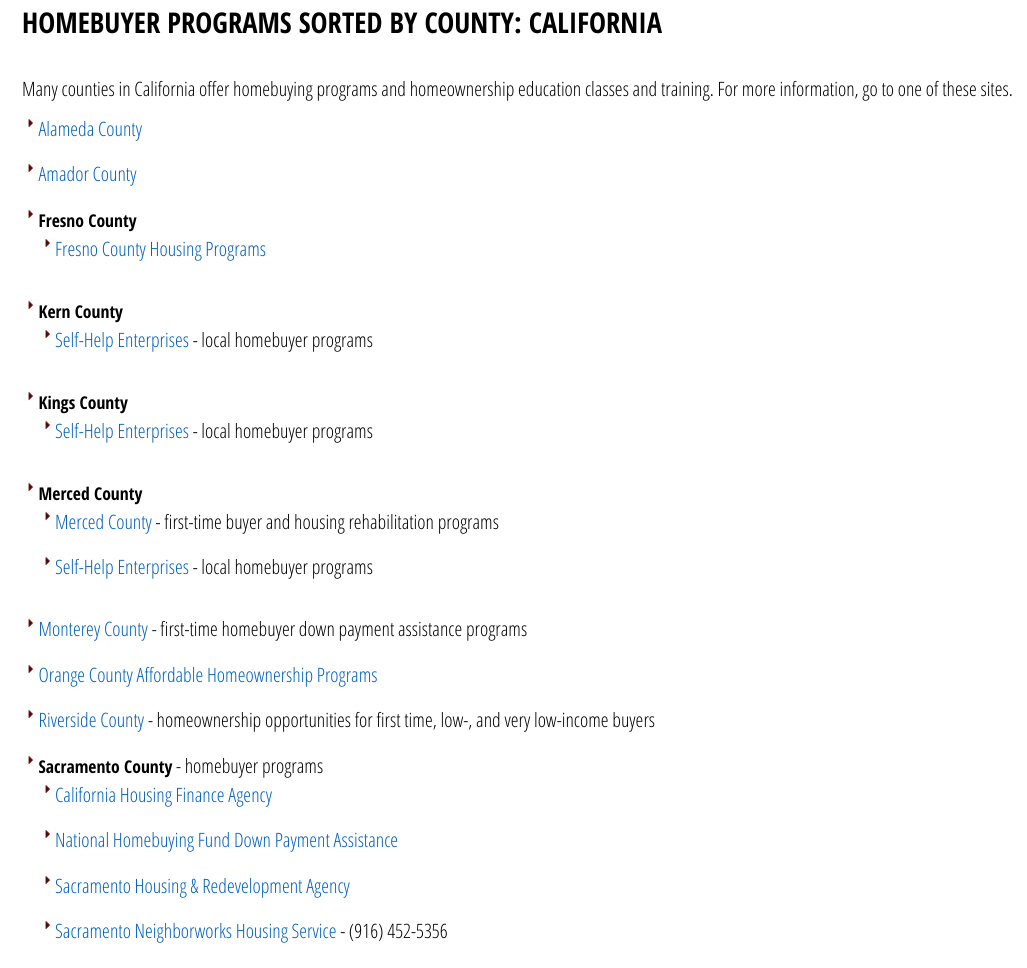

We chose to sort by county, and the following is what came up.

Which counties have first-time home buyer programs? Well… most of them, actually.

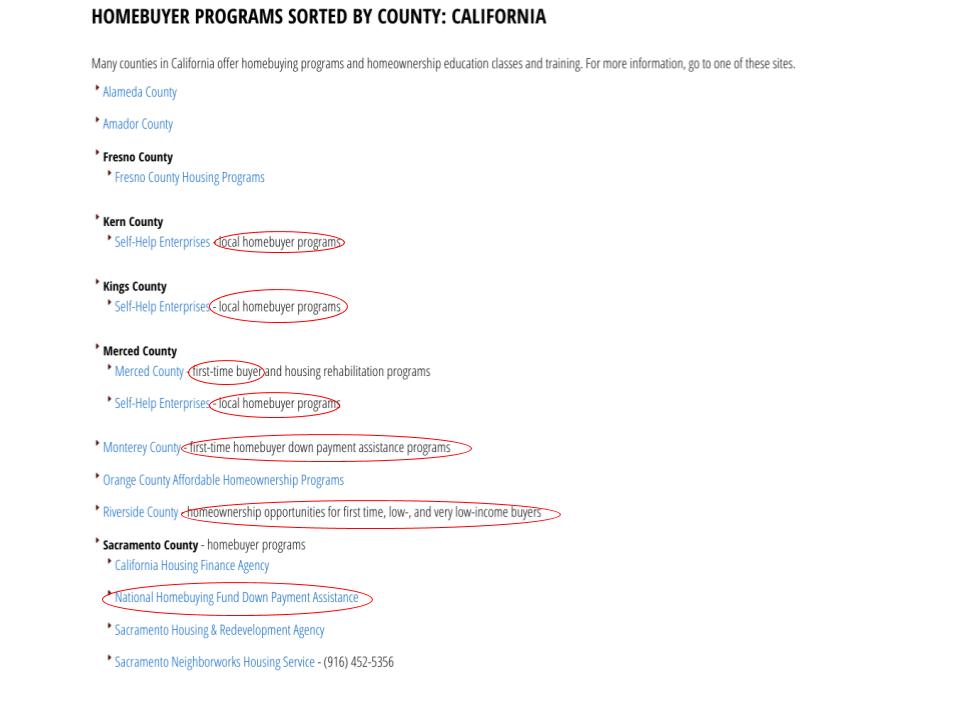

From here it may get a little tricky, but keep digging.

When you click on a county, you’ll be taken to that county’s .gov page. Rarely are you taken right to the home buyer program. Sometimes they’re easy to find and sometimes they’re not. For the most part, counties don’t really advertise that they have home ownership programs in place for their residents. You really have to dig to find them.

If it’s not obvious from the web page where the home ownership program is, you’ll need to click the search button. Try searching with these terms to find the program:

first-time home buyer

first-time homebuyer

home ownership

homeownership

home ownership assistance

homeownership assistance

down payment assistance

downpayment assistance

How each county or city lists it’s program is a little different, so play around with search terms until you find the home ownership program advertised on HUD. As you can see, a lot of search results are skewed because web developers can’t decide which terms are one word or two words. The difference in how these terms are written out often changes search results.

So, if your first few search results don’t yield any results keep trying (HUD did list the county for a reason).

Yes, HUD does make mistakes from time to time, but it’s not often.

Important: HUD often does not list every home ownership program within a state

States are big places, and sometimes not every program is communicated to HUD. California, for example, has a lot of programs listed on its HUD web page, but we found many programs that weren’t listed on HUD (and we do mean many).

So, what do you do if you can’t find one for your area?

Take the search into your own hands. First go to your local government website and try searching for the terms listed above. If you don’t find anything, go to Google and do the same thing.

Start off with a specific area and zoom out as needed, but don’t go beyond your state.

Example:

Midlothian Virginia down payment assistance first time home buyer program (Note: Midlothian is an area within Chesterfield County)

Chesterfield County Virginia down payment assistance first time home buyer program

Virginia down payment assistance first time home buyer program

If you go beyond your state, your search results will likely just yield bank and lender results. Stick with local government programs because these programs are often forgivable loans.

Can non-government programs be trusted?

Some areas will have legitimately good home ownership programs that are not affiliated with local or state governments. Look at the program, read its terms and conditions, and pick up the phone and call if you have any questions. Our advice is to be a little wary of any home ownership program that is run through a bank or lender. Banks make a lot of money off of home loans, and they usually make a few bucks off of down payment or closing cost assistance programs, too.

However, if the program is run through the masons or some other philanthropic organization, give it your time. These programs are usually legitimately good programs for would-be home owners.

What do I do if I don’t find any local programs?

Before you decide that there’s nothing for your area, Google your area + housing department.

Example: Richmond VA Housing Department.

Call and ask to speak with someone who is knowledgeable of home ownership assistance programs. He or she may be able to point you towards a program for your area that is not searchable on the web.

If that doesn’t work, then look into state programs. State programs usually have more applications than local home ownership programs, but that doesn’t mean you would be unlikely to receive any assistance. In general, we recommend local programs over state programs because local programs are likely more tailored for your individual needs. They also sometimes have stricter eligibility requirements.

All in all, don’t write off state programs, but definitely start with local programs first.

Why do lenders not like home ownership assistance programs?

Usually lenders like to know that the money you would use for down payment assistance has come from your own hard work and effort. It’s for this reason that many home ownership programs usually partner with lenders who are willing to accept down payment or closing cost assistance funds. Some programs don’t have lender requirements, but you’ll want to ask your lender if they accept down payment assistance funds. Just because the program is open to working with any lender doesn’t mean your lender will accept funds from an outside source.

If you already have a lender and your lender doesn’t accept home ownership assistance funds, just find one that does. You’re never under any obligation to work with a bank or lender simply because they pre-qualified you. As long as you haven’t closed on the house, you can switch lenders at any time.

Can I apply for a first-time home buyer loan or grant after I’ve put an offer on a house?

With some programs this is OK, but overall we don’t recommend it. The reason is because these programs often take a month or more to simply view your application, and then once you’ve been approved can then take another month to process.

Overall, buying a house with a first-time home buyer loan or grant should be a part of your strategy from the beginning.

How much money do you get with a first-time home buyer program?

It varies state to state and county to county. In high cost areas the assistance will be more than other parts of the country. Funds could be as little as $3,000 to as much as $60,000.

Do you have to be a first-time home buyer?

Usually the fine print says you have to be a first-time home buyer or not have owned a home in the past 3 years. As long as you meet one of these requirements, you are eligible to apply (provided, of course, that you meet the other eligibility requirements).

Do you have to use a certain type of loan?

Rarely do home ownership assistance programs dictate what kind of loan you need to use. More importantly we’ve never seen any discriminate against FHA or conventional loans. So if you want to make a minimum payment of 3.5% with an FHA loan, you can do that and still receive home ownership assistance.

Keep in mind you can also use these programs in conjunction with a USDA or VA loan, both of which don’t require down payments. Doing this would effectively lower the purchase price of your home.

Don’t assume you won’t qualify for a first-time home buyer loan or grant.

There are so many programs out there. Trust us, we know. We’re currently working on a master list for each state that incorporates a list of each program on HUD and and the web (with program specifics listed out so you don’t have to go searching). There are literally thousands upon thousands of home ownership programs in the United States. Do your own search or check out programs for your area in the Down Payment Assistance tab.

If we haven’t gotten to yours yet, just wait. It’s coming. This is one thing we’re definitely passionate about at Hipster Real Estate.